Since Samsung snatched Verizon’s $6.6 billion contract from under Nokia’s nose, it has held a pivotal position in the 5G field. This huge deal was announced in September 2020, when 5G was still young and Nokia was still working on product issues. Encouraged by Verizon’s success and Vodafone’s pursuit in Europe, this South Korean company seems destined to win more deals outside the domestic market.

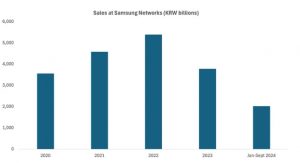

This situation has not completely occurred yet. The sales revenue of Samsung’s network business surged by 29% in 2021, reaching 4.58 trillion Korean won (3.3 billion US dollars), and increased by 18% the following year, reaching 5.39 trillion Korean won (3.9 billion US dollars). But Verzion’s contract did not trigger telecom companies to flock to Samsung. The company’s network revenue decreased by 30% in the cold 5G environment last year, much larger than the 11% market revenue decline calculated by Omdia, sister company of Light Reading. The results show that in the first nine months of 2024, they decreased by 27% year-on-year.

Alok Shah, Vice President of Strategy, Business Development, and Marketing at Samsung Electronics America, said, “But negotiations with existing and potential customers have convinced Samsung that the situation will be much better in 2025. It is confident in Verizon’s accelerated network activity, and the company seems to have yet to complete the transition from Nokia to Samsung at around 10000 mobile sites. They have some quite aggressive C-band construction goals. Next year, Verizon plans to invest $17.5 billion in capital expenditures, up from $17 billion to $17.5 billion in 2024.”

Shah also hopes to earn additional income from Boost Mobile, a brand used by Dish Network. He said, “I believe that Boost, another major customer of Samsung, is improving in terms of overall business strategy and financial condition. The company is building its fourth mobile network across the United States and had previously signed an agreement with Samsung to provide radios and software.”

But in the eyes of many observers, Dish’s financial situation is certainly still unstable. A recent document submitted to the US Securities and Exchange Commission shows that the operational losses of its 5G network deployment have expanded to over $1.7 billion in the first nine months, a year-on-year increase of 46%. At the group level, despite sales reaching $10.7 billion, Dish’s operating loss was as high as $130 million.

Outside of North America, Samsung is also seeking opportunities in Europe. It is widely expected that it will become one of the big winners in Vodafone’s ongoing bidding for tens of thousands of base stations in Europe and Africa. Vodafone has reserved 30% of its European footprint to shift towards open RAN (or O-RAN), with its new interface aimed at facilitating pairing of different vendors on the same mobile site, and Samsung has already appeared in several transactions with Vodafone’s European subsidiary. This includes open RAN deployments in the UK and Romania.

So far, the work of replacing China’s Huawei in about 2500 locations in the UK seems to be progressing slowly. According to a source, only about 100 people have been exchanged so far. The long-term investigation into the merger plan between Vodafone and Three in the UK (referred to by Shah as “external factors”) may have led to the operator seemingly suspending network activities while waiting for a decision. Samsung will benefit from the merger possibly receiving approval early next month.

In other areas of Vodafone’s European infrastructure, Samsung is also actively participating in Germany’s open RAN trials. Shah said, “There must be geopolitical factors in this market. The government has provided guidance to untrusted suppliers, and we believe O-RAN may have a positive impact.”

According to regulations announced this summer, German authorities will allow telecommunications companies to retain Huawei’s 5G base station hardware and software, provided they find a solution to replace this Chinese supplier’s management system. Shah said, “If you look at the demand for open interfaces in network management, you will find that these are some areas of O-RAN development, perhaps not the prequel part, but possibly other aspects of O-RAN.”

These statements indicate that Samsung may be willing to provide a system that can be used to manage Huawei RAN. Ericsson and Nokia may not be willing to play such a role. It can be said that if Germany uses Huawei for a long time, their losses will be greater and they may resist any cooperation with their main competitors, especially when their goal is to ensure Huawei’s presence in the German network.

“The largest operator in Germany, Deutsche Telekom, seems to have developed its own management system for this purpose. But Vodafone seems more interested in guiding suppliers rather than establishing its own Service Management and Organization (SMO) platform. It’s time to influence the direction of things, no matter who you work with,” Paco Pignatelli, Vodafone’s open RAN director, recently told Light Reading.

Shah said he is cautiously optimistic that Germany will develop into an “interesting opportunity” for Samsung. Meanwhile, on the other side of the world, the 5G agreement with Japan’s KDDI (details not yet announced) may also boost sales in 2025.

Not optimistic, Samsung’s market share fell by 1.5 percentage points last year due to the situation in India. As the only 4G RAN product supplier for Reliance Jio, Samsung lost to Ericsson and Nokia when India’s largest telecommunications company awarded a 5G contract. Although Samsung has listed competitors Bharti Airtel and Vodafone Idea as new customers, Samsung’s share in the 5G network coverage of these two companies is still relatively small.

Another risk is that more telecommunications companies choose to develop their own technology or even attempt to sell it. Deutsche Telekom’s SMO program is just one small example. Through a subsidiary called OREX SAI, NTT Docomo in Japan is currently promoting its self-developed SMO platform to other telecommunications companies, including German operators. Competitor SoftBank and chip giant Nvidia have jointly developed their own RAN software. Viettel in Vietnam has also done similar things with Qualcomm. Jio in India has its own core network and hopes to become a 5G product supplier for other telecommunications companies.

But Shah clearly doubts whether these efforts can achieve great success. The things Viettel has done around domestic equipment are indeed very interesting, but I don’t know how big its scale is. There is a reason why we are horizontally divided into service providers and suppliers – it is difficult to vertically integrate and expand our scale in this way.

The market environment next year is still shrouded in uncertainty. Among other things, Donald Trump’s return to the White House may have an impact on telecommunications companies that still rely on Chinese suppliers. But Shah seems determined not to rely too much on external factors. “I think our philosophy has always been that if your business strategy is too closely linked to geopolitical decisions, you may get into trouble.” Regardless of the political weather, if telecommunications companies’ spending declines, difficult times may continue.